The TMS Vendor Consolidation Survival Guide: How to Build Standalone EDI Architecture That Protects Trading Partner Networks from the $2.1 Billion Acquisition Wave Reshaping Transportation Technology in 2026

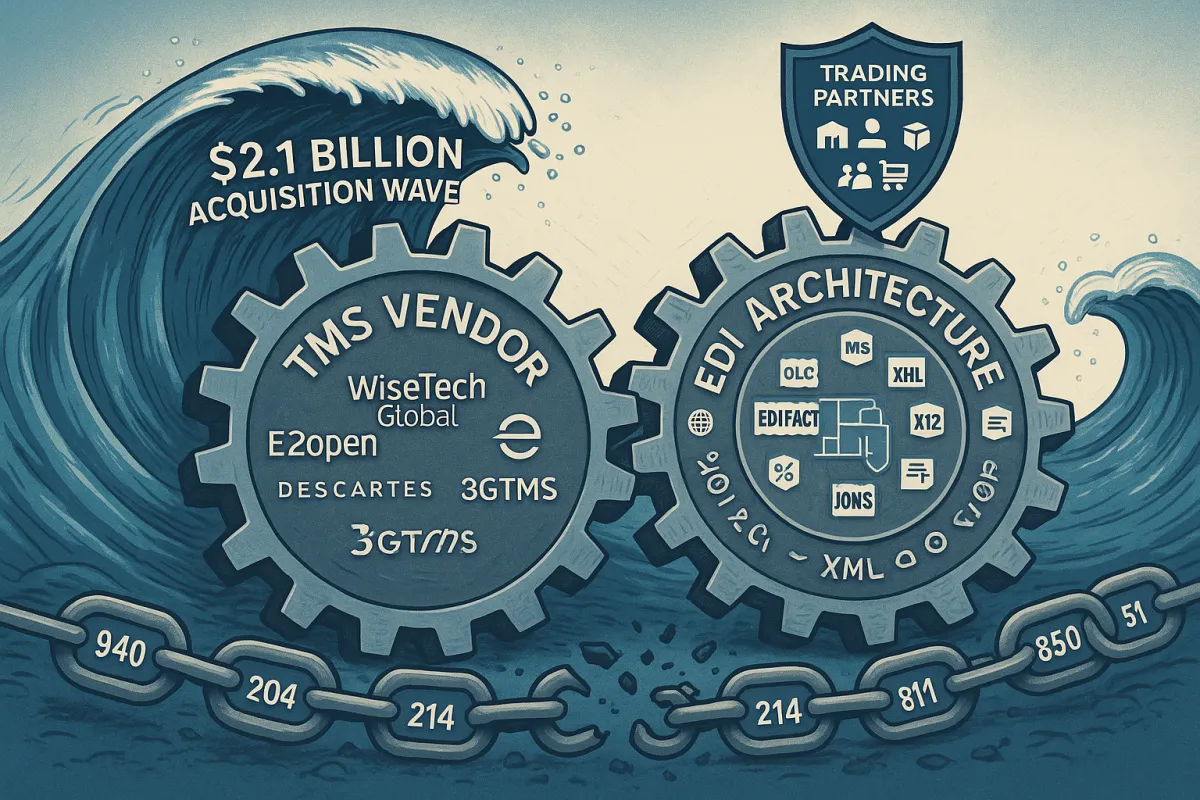

When WiseTech Global's $2.1 billion acquisition of E2open completes in early 2026, along with Descartes Systems Group's acquisition of 3GTMS for USD 115 million in March 2025, thousands of supply chain professionals will discover a harsh reality: their TMS vendor consolidation just broke their EDI connections with hundreds of trading partners.

The problem runs deeper than interrupted data flows. The average company that performs EDI has anywhere from 100-200 partners, and 400-500 maps—all of which will be impacted by the switch when their TMS changes hands. You face delays, chargebacks, or failed deliveries, which can damage partner relationships while new ownership figures out platform consolidation priorities.

The solution isn't avoiding vendor consolidation. The vendor landscape will look dramatically different by 2026, and the TMS market will continue consolidating throughout 2026 and beyond. Instead, you need standalone EDI architecture that protects your trading partner networks regardless of which TMS vendor gets acquired next.

The $2.1 Billion Vendor Consolidation Crisis That's Breaking TMS-EDI Dependencies

This isn't your typical market adjustment. WiseTech Global's $2.1 billion acquisition of E2open and Descartes Systems Group's acquisition of 3GTMS for USD 115 million in March 2025 signal the most significant vendor consolidation wave in TMS market history. Add Körber's transformation of MercuryGate into Infios following their 2024 acquisition, and you're looking at three major platform migrations happening simultaneously.

The deal is supply chain, global trade management and direct importer, exporter, shipper centric, with little overlap between the WiseTech and e2open's largely complementary customers, products and markets. But complementary doesn't mean compatible. When two TMS platforms merge, customers inevitably face decisions about which system to standardize on, what features will be deprecated, and how long dual support will continue.

Here's what happens next: Companies undergoing integration often experience 12-18 months of reduced innovation while they harmonize platforms and teams. Your feature requests get deprioritized. Support quality deteriorates as resources shift toward internal integration projects. Meanwhile, your EDI connections hang in limbo.

Why Traditional TMS-Embedded EDI Creates Fatal Dependencies

The first challenge of EDI inside an ERP, TMS, or WMS is that it will be tightly tied to the ERP. This creates a cascade effect when vendors change hands. Your EDI isn't just processing documents anymore—it's processing documents through a system owned by a completely different company with different priorities.

Consider what TMS-embedded EDI means for critical transactions like 940 warehouse shipping orders, 204 load tenders, and 214 shipment status messages. ERP, TMS, and WMS tend to have very lightweight EDI processing, often requiring multiple additional solutions to handle the complexity. When the underlying TMS changes, everything breaks.

The financial impact compounds quickly. Licensed TMS software runs $50,000-$400,000+ with annual maintenance charges ranging from 15-20% of license costs, with a 100-truck operation's initial $100,000 investment becoming $200,000+ in the first year when factoring in implementation, training, and infrastructure requirements. Vendor acquisitions compound these costs through forced migrations, system re-integrations, and compliance timeline pressures.

The Composable EDI Architecture Solution Framework

Composable EDI architecture treats integration as modular components rather than monolithic systems. Instead of tying EDI processing directly to your TMS, you create interchangeable layers that can survive vendor changes, platform migrations, and technology shifts.

This approach recognizes a fundamental truth: your TMS will change, but your trading partner relationships shouldn't have to. Stay flexible with your integration architecture to accommodate new trading partners and maintain that flexibility when consolidation forces platform decisions on you.

The business case is clear. MasterMind TMS' integration with Orderful eliminates EDI bottlenecks, ensuring smooth, efficient workflows while enabling faster partner onboarding, enterprise-grade performance, and the flexibility to meet client-specific needs. When Mastery Logistics needed to focus on their core TMS capabilities, they offloaded EDI complexity to a dedicated platform that could evolve independently.

Building Vendor-Agnostic Integration Layers

The most resilient architectures use integration Platform as a Service (iPaaS) solutions to create unified data flow management. Instead of point-to-point connections between your TMS and each trading partner, you route everything through a vendor-neutral layer that can interface with any TMS platform.

This strategy proved its value when Tesla abandoned EDI entirely. When Tesla chose to skip EDI in favor of API-based integrations, many carriers found themselves in a bind until vendors like Kleinschmidt created repeatable processes to transform existing EDI data into API-compatible formats.

Modern platforms like Cargoson, Orderful, and Cleo have built their architectures around this principle. They provide domain-specific iPaaS capabilities that understand transportation workflows while maintaining flexibility to adapt as technology evolves.

Implementation Strategy: Decoupling EDI from TMS Dependencies

Start with a complete systems audit. Identify your systems of record—ERP, WMS, TMS, ecommerce platforms—and map how EDI currently flows between them. Before embarking on the integration process, businesses should evaluate their existing TMS and EDI systems. Understanding the current capabilities and limitations will help determine the best approach for integration.

Quantify your EDI volume and complexity. Document every transaction type, trading partner requirement, and custom mapping. This becomes your independence blueprint. The average company that performs EDI has anywhere from 100-200 partners, and 400-500 maps—all of which will be impacted by the switch if you don't decouple properly.

For companies without TMS yet, consider standalone EDI interfaces. We designed a user interface that ultimately acts as a TMS in terms of housing EDI, allowing EDI compliance without TMS dependencies. This means brokers can set up bitfreighter Managed EDI (which can usually be done in days with the help of our Concierge EDI team) and be instantly EDI compliant without the need for a TMS, or without integrating with their existing TMS.

Protecting Trading Partner Networks During Transitions

Your trading partner relationships represent years of investment in onboarding, testing, and operational refinement. This guide explains how to maintain control of your EDI environment during a TMS migration and how a well-planned TMS strategy can support EDI without disruption.

Establish EDI continuity protocols before you need them. Create data export procedures, backup communication methods, and emergency failover processes. When a TMS system is swapped out or reconfigured without an EDI continuity plan, the result is often delays, chargebacks, or failed deliveries, which can damage partner relationships.

Consider hybrid architectures that provide multiple communication paths. Integrating both EDI and API in your TMS is like hitting the sweet spot for your trucking business. EDIs are your go-to for zipping through all those routine business papers, while API is the genius making sure your systems work together seamlessly.

Vendor Selection Criteria for Consolidation-Resistant EDI Platforms

The market now breaks into three categories: global mega-vendors (Oracle TM, SAP TM, E2open/WiseTech), European specialists (Alpega, nShift, Transporeon), and emerging European-native solutions like Cargoson that focus specifically on cross-border European operations.

Evaluate financial stability beyond current revenue figures. While WiseTech has demonstrated consistent profitability and growth, e2open has struggled with financial performance in recent years, reporting declining revenue and net losses in recent fiscal years. Look for vendors with strong balance sheets and diverse revenue streams that can weather market consolidation.

Contract protection becomes essential. Include specific clauses requiring 12-18 months advance notice of ownership changes, with automatic contract review rights triggered by acquisition announcements. Add price protection clauses should lock pricing for 24 months following ownership changes, preventing immediate cost increases during integration periods.

Assess platforms built for modularity. IBM Sterling B2B Integrator, Cleo Integration Platform, and modern solutions like Cargoson prioritize composable architectures that can integrate with multiple TMS platforms simultaneously. This flexibility protects you from vendor lock-in scenarios that force costly migrations.

Future-Proofing Your EDI Strategy for Continued Consolidation

The consolidation wave isn't stopping. Additional acquisitions are likely as private equity firms and strategic acquirers seek to capture market share in the growing European TMS market, requiring procurement strategies that account for ongoing vendor landscape changes. Plan for a market with fewer, larger players who have more control over pricing and feature development.

AI integration opportunities are emerging across EDI workflows. Autonomous agents can now handle real-time optimization, reduce manual troubleshooting, and adapt to trading partner changes without human intervention. But these capabilities require flexible architectures that aren't tied to specific TMS platforms.

Hybrid approaches offer the best long-term protection. Use APIs for real-time status updates and immediate responses, while maintaining EDI for high-volume, complex document exchanges that require audit trails. As Dan Heinen, CEO of Kleinschmidt, pointed out, "The push is going to continue to be digital, digital, digital." Fleets need to embrace this shift to stay competitive.

Modern TMS platforms like Cargoson are already building for this hybrid future, providing both EDI and API capabilities while maintaining vendor independence. Position your EDI strategy to work with multiple platforms rather than depending on any single vendor's roadmap.

The companies that survive the next wave of consolidation will be those that decouple their trading partner relationships from their technology vendor relationships. Build your EDI architecture like you expect your TMS vendor to be acquired tomorrow—because in this market, they probably will be.