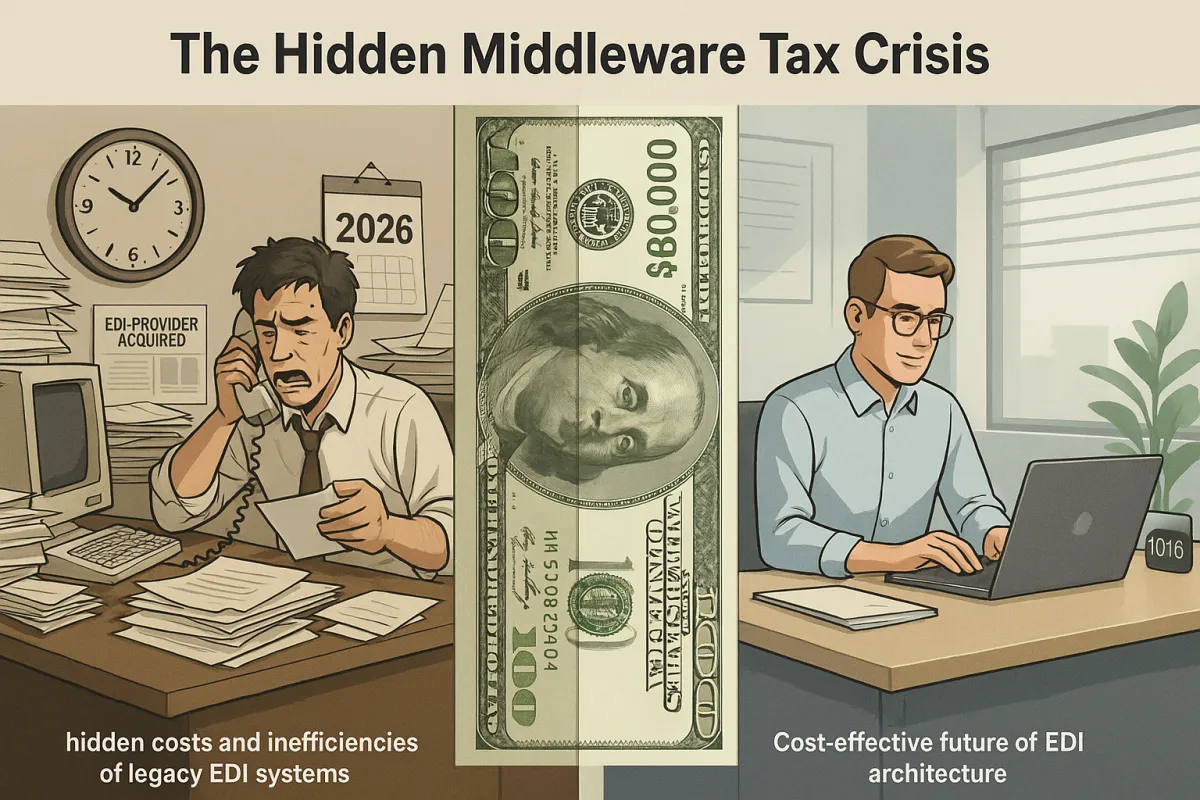

The Hidden $480K Middleware Tax Crisis: Your Complete Cost Assessment Framework to Eliminate Legacy Integration Platform Bloat and Build Vendor-Consolidation-Resistant EDI Architecture That Cuts Total Ownership Costs by 60% in 2026

Your enterprise sits on a $480,000 hidden middleware tax bomb, and most EDI managers don't even know it exists. Hidden Cost: $3,600 – $12,000 / year recurring per integration adds up faster than you think across your trading partner network. While you're debating whether that new carrier relationship is worth the setup fees, legacy translators, batch-based workflows, manual reconciliation, retailer chargebacks, and custom integration maintenance are bleeding operational efficiency every day.

Here's what changed in 2026: WiseTech Global's $2.1 billion acquisition of E2open and Descartes Systems Group's acquisition of 3GTMS for $115 million, marking Descartes' 32nd acquisition since 2016, signal that vendor consolidation is reshaping your negotiating position. The procurement window for securing better terms is closing fast, and organizations that understand the true cost of their current middleware stack hold all the cards in upcoming renewals.

The Middleware Cost Crisis Hidden in Plain Sight

Most EDI teams know their VAN charges and license fees. What they miss is the operational drain that compounds monthly. Legacy EDI setups rely on VAN fees, rigid translator licenses, and heavy engineering maintenance — creating escalating operational costs as transaction volume grows.

The numbers tell the real story: You pay for the implementation of the connector (e.g., Shopify to NetSuite), but you also must pay the annual License Fee for the middleware itself (Celigo, Boomi, FarApp). Hidden Cost: $3,600 – $12,000 / year recurring per integration. A mid-sized manufacturer with 15 trading partner integrations faces $54,000 to $180,000 in annual middleware licensing alone—before counting setup fees, support contracts, or the FTE hours spent troubleshooting batch processing failures.

Sound familiar? That's because Traditional EDI systems operate on scheduled batch windows. Documents are extracted, translated, and transmitted every 15–60 minutes. When something breaks at 2 AM, your team gets the call. When retailers implement new compliance requirements, you're scrambling to update mapping logic across multiple systems. Each manual intervention carries a loaded cost of $85-125 per hour, and most organizations underestimate how often these interruptions occur.

Enterprise service bus platforms like IBM WebSphere and Oracle SOA Suite promised integration simplification but delivered vendor lock-in instead. However, vendor lock-in can be a concern when your middleware strategy depends on proprietary connectors that become more expensive with each contract renewal. Modern platforms like Cargoson, alongside established players like MuleSoft, TrueCommerce, and SPS Commerce, offer transparent per-partner pricing that eliminates these escalation traps.

The Complete Hidden Cost Assessment Matrix

You need a systematic approach to identify where your middleware budget actually goes. Start with licensing fees—the obvious costs—then work through the operational layers that multiply those expenses.

Licensing and VAN Costs: Document your current per-transaction fees, endpoint licensing, and VAN charges. Middleware typically charges based on connections, transaction volume, or feature tiers. The upfront investment runs higher than basic partner solutions, but per-transaction costs stay predictable. Calculate your annual transaction volume across all trading partners and multiply by current per-transaction rates to establish your baseline.

Setup and Integration Fees: Setup fees, custom options, and add-ons can all add to the actual cost of the tool. Also, if you'll need to get your own developers involved, you'll need to factor in the cost of their time and resources. For NetSuite integrations specifically, third-party connectors or middleware platforms (e.g., Celigo, Boomi, Dell Boomi) carry their own licensing fees, typically $5,000–$50,000+ annually depending on integration complexity and data volume.

Beyond Software Licenses - The Operational Drain

Manual intervention costs destroy your middleware ROI faster than licensing fees. At $25/hour loaded cost, you're spending $52,000+ annually just on order entry. A single late or incorrect advance ship notice results in $100-$500 chargebacks from major retailers. If you're getting chargebacks monthly, that's $1,200-$6,000+ annually per trading partner.

Mapping errors create the biggest hidden expense. When your EDI translator can't handle a retailer's optional field variations or fails to validate business rules before transmission, the downstream costs multiply: chargeback penalties, customer service calls, rush shipments to replace incorrect orders, and the staff time to investigate and resolve each issue.

Structured data reduces reliance on specialized EDI technicians and lowers support costs when systems parse documents directly into databases instead of treating EDI as flat files. This architectural difference explains why modernizing the integration layer, not replacing core systems, is typically the fastest way to cut costs by 30–60%.

Vendor Consolidation Impact on Middleware Economics

The TMS vendor consolidation wave is reshaping middleware economics in ways most EDI managers haven't considered yet. This aggressive acquisition pattern indicates further consolidation ahead, not behind us. WiseTech Global's $2.1 billion acquisition of E2open is more than a headline—it's a directional shift for one of the industry's biggest technology players.

Here's what this means for your middleware costs: fewer independent vendors, reduced competitive pressure, and integration priorities that favor the acquiring company's existing customer base over new requirements. Pricing typically increases 18-24 months post-acquisition once integration costs are absorbed. The newly combined entity faces less competitive pressure, particularly if the acquired vendor held significant market share in specific geographies or verticals.

Consider how vendor acquisitions introduce operational uncertainty that extends well beyond the initial integration period. Service levels often decline during the 12-18 months following acquisition as resources focus on technical integration rather than customer support. When your middleware provider becomes distracted by platform consolidation, you inherit delayed feature updates and longer response times without direct control over the situation.

The procurement leverage you have today disappears when consolidation eliminates your backup options. Companies that haven't initiated TMS selection processes by mid-2026 will find significantly fewer viable options as consolidation eliminates redundant platforms. This dynamic applies to middleware vendors as well—establish alternative relationships before your current vendor becomes an acquisition target.

Modern Alternatives That Cut Costs by 60%

API-first platforms fundamentally change middleware economics by eliminating per-transaction fees and VAN dependencies. Modern real-time integration reduces or eliminates recurring VAN expenses, minimizes custom ERP work, and shifts infrastructure to scalable cloud subscriptions.

The cost difference is substantial. Traditional ESB implementations require specialist knowledge to maintain custom connectors and translation maps. Modern integration partnerships replace that model with predictable pricing and managed automation, so your IT and finance teams can budget with confidence. Automation also minimizes the human element that leads to costly errors or compliance gaps.

Real-world implementations show the math. Modern EDI platforms make NetSuite EDI integration affordable for small businesses through flat per-partner pricing starting at $399/month. Web EDI options start at $189/month per trading partner for companies processing lower volumes. Compare that to traditional middleware where Hidden Cost: $3,600 – $12,000 / year recurring per integration creates unpredictable budget escalation.

The Business Case for API-First Integration

Moving to real-time EDI processing reduces chargebacks, eliminates duplicate manual adjustments, and improves retailer scorecards. When systems remain synchronized continuously, documents reflect current data instead of outdated snapshots.

Orderful provides API-first EDI that connects directly to NetSuite, eliminating middleware and accelerating partner onboarding. Alongside platforms like Cargoson, SPS Commerce, and TrueCommerce, these solutions demonstrate how P2P middleware pulls the required P2P platform connections onto a single integration layer, combining these connections into one SaaS solution, as opposed to multiple, thus significantly saving on costs. Automating the data exchanges between parties, as well as feeding this data into the correct endpoints, also removes a number of time-consuming and error-prone manual processes.

The implementation timeline advantage matters when vendor consolidation creates urgency. Cloud TMS implementations often conclude within eight weeks, compared to 6-18 months for traditional systems. This speed difference becomes crucial when your current vendor announces acquisition plans and you need operational alternatives quickly.

Implementation Strategy - Phase-Out Without Disruption

You can't replace your entire middleware stack overnight without risking trading partner relationships. The recommended approach shifts from comprehensive platform evaluation to phased implementation with multiple vendor relationships. Start with one major shipping lane, measure results over 6-9 months, then expand systematically.

Begin with your newest trading partners or those requiring minimal customization. Onboarding major retailers happens in days because the connections already exist. Your team doesn't build Walmart's EDI specifications from scratch; the partner has them ready on modern platforms.

Run parallel systems during transition periods to minimize risk. Keep your legacy middleware operational for established partners while new integrations use API-first platforms. This dual approach protects revenue while demonstrating cost savings on new implementations. Document the performance differences—response times, error rates, manual intervention requirements—to build the business case for broader migration.

Training requirements differ significantly between traditional middleware and modern platforms. Structured data reduces reliance on specialized EDI technicians and lowers support costs because business users can understand parsed database records more easily than flat EDI files. Plan for this skill set transition in your implementation timeline.

Building Consolidation-Resistant Architecture

Design your integration architecture to survive vendor acquisitions and market changes. Avoid vendor lock-in whenever possible by selecting platforms that support industry-standard APIs and data formats rather than proprietary connectors.

Contract protection clauses become essential in a consolidating market. Acquisition-resistant contracts require specific protections including 12-18 months advance notice for ownership changes, guaranteed functionality preservation for minimum periods, and migration assistance rights. Include these terms in new vendor negotiations—they cost nothing when the vendor is stable but provide crucial protection if acquisition discussions begin.

Multi-vendor strategies reduce single-point-of-failure risks. Instead of routing all integrations through one middleware provider, distribute critical trading partners across platforms like Cargoson, Orderful, and established providers like Descartes or MercuryGate. Leverage competitive dynamics between Oracle TM, Blue Yonder, Manhattan Active, Descartes, and independent players like Cargoson. The post-consolidation landscape reveals three distinct categories: global mega-vendors (Infios/MercuryGate, Descartes, SAP TM, Oracle TM, E2open/WiseTech), European specialists (Alpega, nShift, Transporeon/Trimble), and emerging API-first platforms.

Your middleware architecture should support both current EDI requirements and future API transitions. Modern integration partners bridge the gap between legacy EDI systems and real-time APIs, giving you the best of both worlds. You can maintain the reliability of established EDI workflows while connecting to newer, cloud-native applications through APIs within a single platform.

The window for securing consolidation-resistant middleware architecture closes as vendor options narrow. The procurement window for securing optimal TMS platforms before vendor consolidation eliminates choices and capacity shortages worsen cost structures runs through Q1 2026. After this window closes, three dynamics work against European shippers. First, Europe's driver shortage is projected to triple by 2026 if no action is taken, creating capacity constraints that shift pricing power toward carriers and their technology partners.

Take action now while competitive dynamics still favor buyers. Document your current middleware costs, establish relationships with multiple platform providers, and negotiate contracts that protect against post-acquisition changes. The organizations that move decisively in the next 90 days will control their integration destiny. Those that wait will pay premium pricing for fewer options in an increasingly consolidated marketplace.